Coding

PySVAR

This is a mini package (or just call it a bag-of-codes) designed for SVAR estimation across multiple identification schemes. I named it PySVAR, just trying to keep up with the Python package naming trend. It’s super straightforward—there will be virtually no learning curve if you’re familiar with Sklearn. Simply input the parameters, and all set!

You can find the code here.

Usage

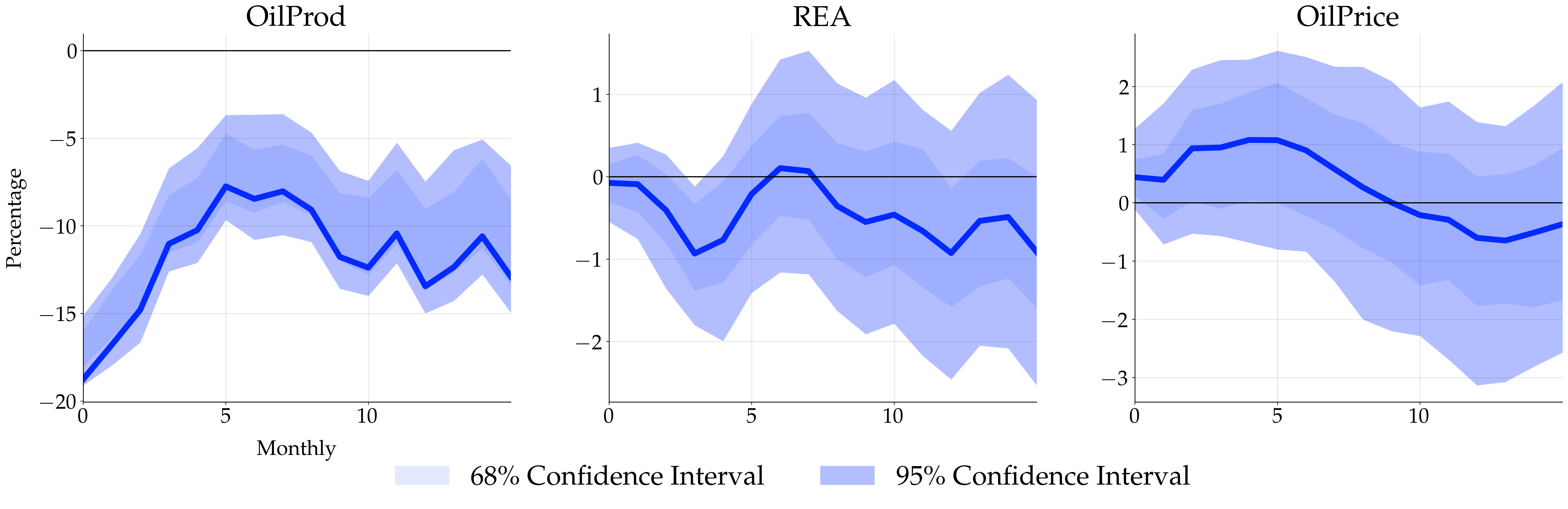

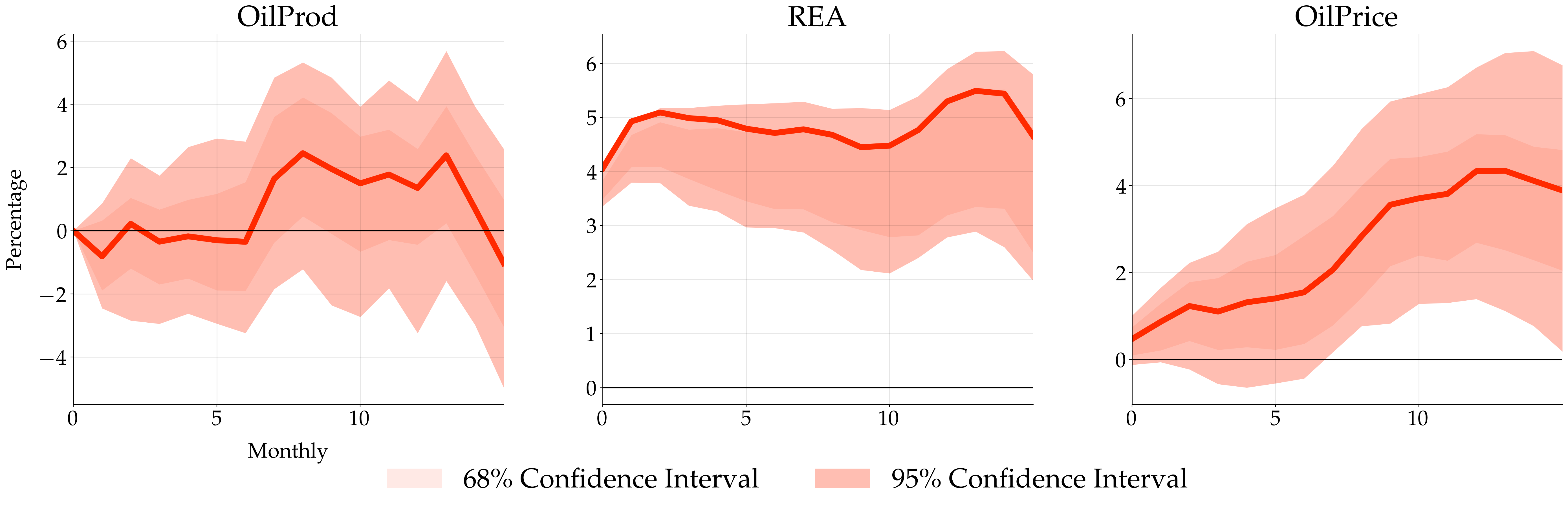

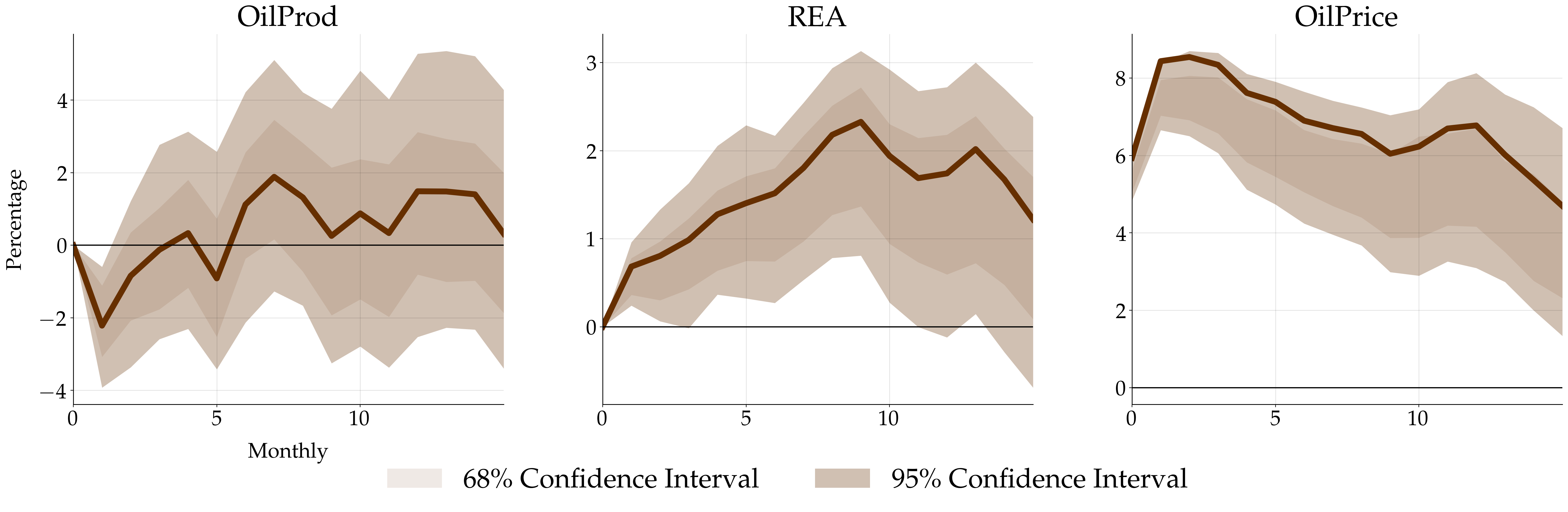

We begin with one of the simplest possible identification method: the Cholesky identification, used by Kilian in the 2009 AER paper. Assuming $e_t=A_0^{−1}\epsilon_t$, where $e_t$ represents the reduced form errors and $\epsilon_t$ denotes the structural shocks and $A_0^{-1}$ is defined as

\[e_t=\begin{pmatrix} e_t^{\Delta\text{prod}}\\ e_t^{\text{rea}}\\ e_t^{\text{rop}} \end{pmatrix}=\begin{bmatrix} a_{11} & 0 & 0\\ a_{21} & a_{22} & 0\\ a_{31} & a_{32} & a_{33} \end{bmatrix}\begin{pmatrix} \epsilon_t^{\text{oil supply shock}}\\ \epsilon_t^{\text{aggregate demand shock}}\\ \epsilon_t^{\text{oil specific-demand shock}} \end{pmatrix}\]To model the above problem,begin by importing RecursiveIdentification. Next, create an instance, utilizing the appropriate parameters

from identification.recursive_identification import RecursiveIdentification

n = ['OilProd', 'REA', 'OilPrice']

s = ['Supply', 'Agg Demand', 'Specific Demand']

recr = RecursiveIdentification(data=o, var_names=n, shock_names=s, lag_order=24, date_frequency='M')

Once the instance is initialized, invoke .identify() for estimation and .bootstrap() to calculate the confidence interval

recr.identify()

recr.bootstrap(seed=3906)

After identification, one can use .irf() or .vd() to calculate the impulse responses and variance decomposition, respectively. Similar to the approach taken by Kilian in his paper, I also calculate the cumulative response of $\Delta \text{prod}$ as follows:

mdls = [recr]

for m in mdls:

m.irf_point_estimate[0, :] = -np.cumsum(m.irf_point_estimate[0, :])

m.irf_point_estimate[3, :] = np.cumsum(m.irf_point_estimate[3, :])

m.irf_point_estimate[6, :] = np.cumsum(m.irf_point_estimate[6, :])

m.irf_point_estimate[1, :] = -m.irf_point_estimate[1, :]

m.irf_point_estimate[2, :] = -m.irf_point_estimate[2, :]

for _ in range(m.irf_mat_full.shape[0]):

m.irf_mat_full[_, 0, :] = -np.cumsum(m.irf_mat_full[_, 0, :])

m.irf_mat_full[_, 3, :] = np.cumsum(m.irf_mat_full[_, 3, :])

m.irf_mat_full[_, 6, :] = np.cumsum(m.irf_mat_full[_, 6, :])

m.irf_mat_full[_, 1, :] = -m.irf_mat_full[_, 1, :]

m.irf_mat_full[_, 2, :] = -m.irf_mat_full[_, 2, :]

m.plot_irf(h=15, var_list=n, sigs=95, with_ci=True)

where the point estimate and confidence interval are stored in irf_point_estimate and irf_mat_full, respectively. Lastly call .plot_irf() to plot the impulse response. Here is the plot (supply shocks, aggregate demand shocks, and specific demand shocks):

Versions

The current beta version now includes sign restriction, recursive identification, exclusion identification, and some bayesian models. I will continue to update the package

The next version will include identification through heteroscedasticity. It will also incorporate historical decomposition.

Jan 2024 update: Support for parallel computing has been implemented for sign restrictions, resulting in a 50% speed increase.

May 2024 update: Support for optimization based identification method.

June 2024 update: Support for several priors.

Disclaimer

This is a beta version. The code has not undergone extensive testing as of yet. While I hope it proves useful, I provide absolutely no guarantees, either expressed or implied, regarding its functionality or suitability for your needs.

Thanks

I wish to extend my deepest thanks to my advisor, Dr. Marco Brianti, for introducing me to this field and for providing generous guidance on the SVAR model’s identification and estimation techniques.